OCCU-TEC, Inc.

OCCU-TEC, Inc.

Courtesy of Summit, a Liberty Mutual Company

Returning injured employees to work has become more and more important in controlling claims costs. However, it is easy to think that you don't need a formal return-to-work program—until it's too late.

Dollars and sense

No matter how safe a business strives to be, accidents can still happen. The National Safety Council reports that a disabling injury occurs every 1 second in the U.S. (more than 63,000 every day), and the Social Security Administration predicts that 1 out of 4 workers entering the workforce today will acquire some type of disability before they retire.

The current economic climate and its subsequent effect on employment have called attention to the importance of doing what it takes to get employees back to work as quickly as possible. Research consistently shows that injured employees recover faster, are more satisfied with their care, return to their full-duty positions sooner, and are released from medical care earlier if they work for companies that offer transitional duty. Effective return-to-work programs can also cut workers' compensation premium costs, so you have some solid reasons to implement your own program.

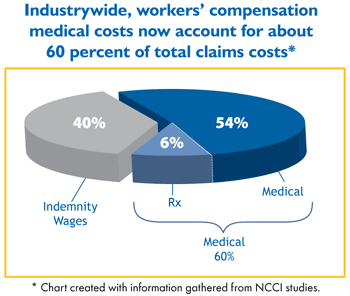

Comp claims cost more now than ever before. The National Safety Council reports that a single work-related disabling injury costs an average of $48,000. The National Council on Compensation Insurance (NCCI) estimates that the medical costs are currently about 60 percent of the overall cost of a lost-time claim—and climbing. As an employer, you cannot control the high medical and pharmaceutical costs driving this hike, but you can affect the other cost—indemnity—which is the cost of paying an employee (who may be well enough to work at a modified or alternate job) to stay at home. A strong return-to-work program allows you to control this part of your comp dollars—and could impact the medical portion as well.

It may seem counterintuitive to pay injured employees their salary for modified or alternate work (especially because this type of work can carry a perception of decreased productivity), but the alternative is to let them use their workers' comp benefits to earn a nearly full salary—for zero productivity. More, the American College of Occupational and Environmental Medicine (ACOEM), points out that the odds of an injured employee ever returning to work drop by 50 percent at the twelfth week of disability. A claim lasting that long could affect your workers' compensation premium for several years.

Legal matters

Increased protection from litigation is another significant benefit for offering medically appropriate alternate work. Offering a job puts you in a much stronger position because it's tough to argue that an employee who rejected a reasonable offer to return to work should expect to receive long-term work comp benefits. Without a return-to-work job offer, the odds of having a judge remove an employee from workers' comp benefits drops significantly. In a nutshell, employers who routinely make good faith job offers have stronger results in court.

A 2010 study by the Workers Compensation Research Institute found that workers are more likely to seek legal help when they feel threatened. Since return-to-work programs offer assurance to employees that their jobs are available, they are a huge plus. They also help combat fraud and provide timely, positive communication. According to the California Workers' Compensation Institute, calling injured employees within a week after an accident to talk about their value to the company reduces the chance of a lawsuit by 50 percent. Those are odds worth cultivating.

Upcoming mod changes

NCCI uses a complex formula that spreads the cost of loss through members of an industry likely to experience similar workers' compensation injuries. For fairness, they apply the formula to each company's actual payroll and loss data over the prior three-year period to create an experience modification factor (mod). A 1.00 mod means you had the expected number of accidents, and you pay the average rate. You could pay less if your mod is lower than 1.00. Companies with a higher loss history (resulting in a higher mod) pay more in premium. And since the cost of an accident is less predictable than the frequency, NCCI has long given greater weight (and penalty) to companies that suffer multiple accidents versus those who might have one large claim. However, a significant change to this process—the first in 25 years—is on the horizon.

The anticipated change in NCCI's mod calculation—if approved—is proposed to begin rolling out in 2013. It is a gradual, three-year increase intended to compensate for the jump in overall claim expenses in the past years. The new formula will impact claims differently so that a company with several small losses actually receives a higher mod than a company with a single, larger loss.

The goal that employers will want to shoot for is safe workplaces and a mod of 1.00 or lower. And one significant way to get there is to implement a solid return-to-work program now—before an accident happens.

The time is now

The short story is that it's worth the effort to find light-duty positions for injured workers while they recover. Having a return-to-work program gives you a tool to manage your workers' comp costs, and it's the one variable you can control in this ever-changing economy. The small up-front costs beat the potential landslide of long-term claim-related expenses.